Consider a gold bullion dealer in Bangkok whose vault holds $3 million in stock at any given time. Consider a diamond merchant in Antwerp who entrusts a parcel of loose stones worth $500,000 to a courier for delivery to a client in Singapore. Consider a family-owned jewellery house in Mumbai that sends its most exquisite pieces to an exhibition in Hong Kong, displayed in temporary showcases under temporary security in a convention centre thousands of kilometres from home.

Each of these scenarios involves assets of extraordinary value, high portability, and universal desirability, moving through environments of varying security. The risks are unlike anything in conventional property or marine insurance. The goods are small enough to conceal, valuable enough to attract sophisticated criminal attention, and difficult enough to identify that a stolen diamond can be recut and resold within days. The valuation of a single item can be subjective, contested, and dependent on market conditions that fluctuate by the hour.

This is the world of Jewellers Block and Specie insurance: one of the oldest, most specialised, and least understood classes of coverage in the global insurance market. It is a world where the underwriter must understand not just insurance principles but the jewellery trade itself, its rhythms, its vulnerabilities, its customs, and its culture of trust.

In this final instalment of the Insurance Decoded series, we will explore what Jewellers Block insurance is, what it covers, how it differs from standard property and marine policies, how claims are managed, and why technology is transforming the way the trade's most precious assets are protected.

What is Jewellers Block Insurance?

Jewellers Block insurance is a specialised form of all risks coverage designed specifically for businesses in the jewellery, precious metals, and gemstone trade. The name “Jewellers Block” is a historical term derived from the concept of insuring the entire “block” of a jeweller's stock under a single policy, rather than insuring individual items or individual transit shipments separately.

What makes Jewellers Block distinctive is its breadth. A standard property insurance policy covers goods at the insured premises. A standard marine cargo policy covers goods in transit. A Jewellers Block policy covers the jeweller's stock in trade against all risks of physical loss or damage, regardless of where that stock is located, subject to the territorial limits and conditions of the policy.

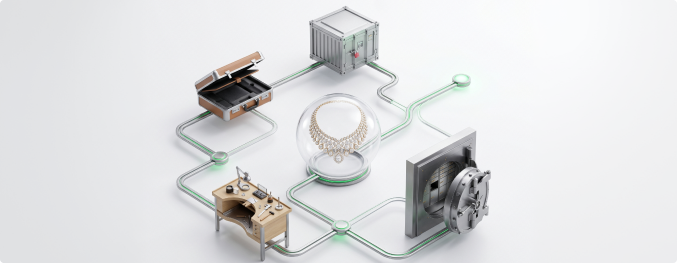

This means the policy covers stock on the insured's premises (in the showroom, in the vault, in the workshop), stock in transit (between the jeweller's premises and clients, between cities, between countries), stock at trade exhibitions and fairs, stock in the hands of sales representatives travelling to meet clients, stock held by third parties for repair, valuation, or consignment, stock being processed by manufacturers, setters, or polishers, and in many cases, stock held at the jeweller's private residence. This last point is particularly relevant in Southeast Asia, where family-owned jewellery businesses frequently store high value items at the owner's home overnight or over weekends, blurring the line between commercial premises and personal residence.

For a trade where stock is constantly moving, being displayed, being entrusted to third parties, and crossing international borders, this all-encompassing coverage is not a luxury. It is an operational necessity.

What Jewellers Block is Not

It is important to clarify a common misconception. Jewellers Block insurance is not a retail product sold to individuals who own jewellery. It is a commercial insurance product for businesses in the jewellery trade. A consumer who wants to insure an engagement ring or a family heirloom would typically do so through a personal articles policy or a homeowner's insurance extension. Jewellers Block insures the trade, not the consumer.

Specie Insurance: The Broader Category

Jewellers Block sits within a broader insurance class known as “Specie.” If Jewellers Block can be thought of as the “static shield” (protecting stock wherever it sits), then Specie insurance is the “moving shield”: covering high value, portable assets with a particular emphasis on transit and secure storage. The word “specie” originally referred to coin and bullion, but the class has expanded to encompass a wide range of valuable property.

What Falls Under Specie?

Gold, silver, platinum, and other precious metals in bullion, bar, or coin form. Cut and uncut diamonds, gemstones, and pearls. Finished jewellery, watches, and luxury goods. Fine art, antiques, and collectibles. Cash in transit and vault storage. Museum and exhibition contents. Private collections of wine, classic cars, or rare manuscripts.

The common thread is that specie items are high in value relative to their size, globally mobile, attractive targets for theft, and often difficult to value accurately. These characteristics demand underwriting expertise that goes far beyond standard property or cargo insurance.

Money Services Businesses: The Underserved Market

One of the most significant segments within specie insurance is the Money Services Business (MSB) sector: money changers, remittance operators, pawnbrokers, and cash handling businesses. For decades, general insurers have largely declined to cover MSBs because they lack the expertise to model the specific risks involved: employee fraud during cash handling, armed robbery of premises, theft during cash in transit operations, and the difficulty of verifying cash volumes.

This has left many MSBs, particularly smaller operators in Southeast Asia, either uninsured or reliant on inadequate security measures. The gap is significant because these businesses are essential to the financial infrastructure of their communities, particularly in markets where large segments of the population remain underbanked. Specialist specie insurers and Coverholders who understand the MSB risk profile are beginning to close this gap, but insurance penetration in the sector remains low.

Specie vs. Standard Property and Marine Insurance

Understanding why the jewellery trade cannot rely on standard insurance policies is fundamental to understanding why Jewellers Block exists as a separate class.

Standard property insurance is designed for assets that are stationary: buildings, equipment, inventory sitting on shelves. It covers perils at a defined location. The moment goods leave the premises, standard property coverage typically ceases or becomes severely limited.

Standard marine cargo insurance covers goods in transit between defined points. It is designed for shipments: goods that leave point A and arrive at point B. Once the goods arrive and are unpacked, the marine coverage ends.

The jewellery trade operates in the spaces between these two categories. Stock moves constantly. A single parcel of diamonds might be examined at the jeweller's premises in the morning, sent to a setter across town in the afternoon, returned the following day, placed in a sales representative's bag for a client meeting the next week, and then shipped to an exhibition overseas the week after. At no point does the risk fit neatly into the standard property or standard marine framework. Jewellers Block was created precisely to close this gap.

The Unique Risks of the Jewellery Trade

To appreciate the complexity of Jewellers Block underwriting, one must understand the specific risks that the trade faces.

Theft and Robbery

Jewellery is, by its nature, one of the most theft-attractive asset classes in the world. It is small, portable, universally valuable, and relatively easy to conceal. The jewellery trade faces threats ranging from opportunistic shoplifting to sophisticated, planned robberies by organised criminal groups. Armed robbery of jewellery premises, smash-and-grab raids on display windows, and theft from couriers and sales representatives are all claims scenarios that Jewellers Block underwriters see regularly.

The challenge for underwriters is that security measures can mitigate but never eliminate theft risk. A vault with a Class XI rating, CCTV cameras, armed guards, and restricted access procedures is more secure than a retail display case, but even the most fortified premises have been breached. The underwriter must assess the quality of the insured's security infrastructure and the adequacy of their operational protocols, and price the risk accordingly.

Transit Risk

Every time jewellery moves, it is at its most vulnerable. Transit creates opportunities for theft, loss, and damage that do not exist when goods are in a controlled environment. The risks are varied and sobering: armed robbery of couriers, hijacking of vehicles carrying consignments, collusion by courier employees with criminal networks, loss or pilferage during air freight handling, and damage from mishandling of fragile items. These are not theoretical scenarios; they are claims that occur with regularity across the global jewellery trade.

The risk profile varies enormously depending on the mode of transit (hand carry by trusted staff, registered post, armoured vehicle, commercial air freight), the route (domestic vs. international, stable vs. unstable jurisdictions), the value of the consignment, and the security measures in place. Underwriters assess transport mode, shipment frequency, maximum carrying limits per transit, routing geography, and whether the insured uses established secure logistics providers.

International transit introduces additional complexity: customs declarations, temporary importation permits, varying regulatory requirements, and the involvement of multiple handlers across multiple jurisdictions. A parcel of gemstones shipped from Sri Lanka to Geneva may pass through three countries, four courier companies, and two customs regimes before reaching its destination. Each handover point represents a moment of elevated risk.

Exhibition and Trade Fair Risk

Trade exhibitions are a cornerstone of the jewellery industry. Events like the Hong Kong Jewellery and Gem Fair, Baselworld, JCK Las Vegas, and the Bangkok Gems and Jewelry Fair bring together thousands of exhibitors and buyers in temporary venues with temporary security arrangements. The concentration of high value goods in a single location, often displayed in glass showcases rather than secure vaults, creates a unique risk profile.

Underwriters assess exhibition risk based on the venue's security arrangements, the insured's own display security measures, the duration of the exhibition, and the transit arrangements before and after the event. Exhibition extensions within Jewellers Block policies often carry specific conditions regarding overnight storage, showcase specifications, and the presence of attendants during display hours.

Employee Dishonesty and Infidelity

One of the most painful risks for any jeweller is theft by a trusted employee. In a trade built on personal trust, where valuable goods are handled by staff on a daily basis, employee dishonesty can cause devastating losses. A workshop employee who systematically substitutes genuine stones with synthetic ones. A sales representative who diverts client payments. A vault manager who manipulates stock records to conceal missing inventory. These scenarios are not hypothetical; they represent a significant proportion of Jewellers Block claims.

Policies typically include employee dishonesty or fidelity coverage, but the conditions are important. There may be waiting periods before discovery, limits on the maximum amount recoverable per employee, and requirements for stocktaking procedures and internal controls. The insured's governance practices are as important to the underwriter as their vault specifications.

Mysterious Disappearance

Few concepts in insurance are as contentious as mysterious disappearance. This refers to the loss of stock where there is no evidence of theft, no evidence of damage, and no explanation for the shortfall. A stocktake reveals that a parcel of diamonds that should be in the vault is simply not there. There is no broken lock, no alarm activation, no suspicious CCTV footage. The goods have vanished.

Some Jewellers Block policies cover mysterious disappearance; others explicitly exclude it. Where it is covered, it is typically subject to a higher deductible and strict stock record-keeping requirements. The insured must demonstrate a rigorous, documented system for tracking the movement and custody of every item. Without this discipline, a mysterious disappearance claim becomes virtually impossible to substantiate.

Valuation and Market Fluctuation

Unlike most insured assets, the value of jewellery and precious goods is subjective, variable, and dependent on specialist expertise to determine. A diamond's value depends on the 4Cs (carat, colour, clarity, and cut), on market conditions at the time of loss, and on the opinion of the appraiser. Gold and platinum prices fluctuate daily. Antique and period jewellery carries values that are part material, part craftsmanship, and part provenance.

This valuation complexity creates challenges for both underwriting (setting the correct sum insured) and claims (agreeing the value of lost or damaged items). The principle of indemnity demands that the insured is restored to their pre-loss position, but determining that position requires specialist knowledge that generalist loss adjusters simply do not possess.

Moral Hazard: The Invisible Risk

Moral hazard is a concept that runs through all insurance, but it is particularly acute in the jewellers block class. The portability, concealability, and high value of insured goods create inherent temptations that underwriters must account for.

Moral hazard in this context does not necessarily mean deliberate fraud (though that exists). More commonly, it manifests as relaxed security discipline once a policy is in place, inadequate stock record keeping that makes it impossible to verify losses accurately, overvaluation of stock to inflate potential claims, or the gradual erosion of operational controls when the owner believes the insurer will bear any loss.

Underwriters manage moral hazard through a combination of strict disclosure requirements at inception and renewal, security warranties that the insured must comply with as a condition of coverage, periodic stock audits and security surveys, geographic limitation clauses that restrict coverage to approved territories, and maximum values per location and per transit that limit the insurer's aggregation exposure. Operational discipline is not just good business practice for a jeweller. It is a condition of insurability. The insured who maintains rigorous security, meticulous records, and transparent reporting is rewarded with stable coverage and competitive terms. The insured who does not will eventually find coverage unavailable at any price.

Inside the Policy: Key Coverage Features

All Risks Basis

Jewellers Block policies are written on an all risks basis, meaning they cover all risks of physical loss or damage unless specifically excluded. This is the broadest form of coverage available and places the burden of proof on the insurer to demonstrate that an exclusion applies, rather than requiring the insured to prove that a named peril caused the loss.

Territorial Scope

Policies define the geographical territory within which coverage applies. For a local retailer, this might be a single country. For an international trading house, the territorial scope may extend across Asia, Europe, the Middle East, and beyond. Getting the territorial scope right is critical. A shipment to a country not covered by the policy leaves the goods entirely uninsured during that transit.

Basis of Valuation

Policies specify how losses will be valued. Common bases include replacement cost (the cost of replacing the item with one of similar kind and quality), agreed value (where the insurer and insured agree on a value at inception, which is paid in the event of a total loss), and market value at the time of loss. The choice of valuation basis can have a significant impact on claims settlements and should be carefully considered at the time of policy placement.

Security Warranties and Conditions

Jewellers Block policies contain detailed security requirements that the insured must comply with as a condition of coverage. These typically include specifications for safes and vaults (minimum ratings, locking mechanisms, bolt work), alarm systems (type, monitoring arrangements, response protocols), CCTV requirements, access control procedures, and protocols for carrying stock outside the premises. Non-compliance with security warranties can void the policy for any related claim, making it essential that the insured understands and adheres to every condition.

Pairs, Sets, and Partial Loss

Jewellery frequently exists as part of a pair or set (earrings, cufflinks, matching necklace and bracelet sets). If one item from a pair or set is lost or damaged, the diminution in value of the remaining items can be significant. A single earring from a matched pair of rare Kashmir sapphire earrings may be worth a fraction of what the pair was worth together. Policies address this through pairs and sets clauses, which define how the insurer will compensate for this diminution.

Claims in Jewellers Block: A Specialist Process

Claims in Jewellers Block insurance are among the most complex in the specialty insurance market. They require specialist adjusters, specialist valuers, and a deep understanding of the trade's practices.

The Claims Process

When a loss occurs, the insured must notify the insurer immediately and take all reasonable steps to prevent further loss or damage. In the case of theft, a police report must be filed. The insurer appoints a loss adjuster, ideally one with experience in jewellery and precious goods claims, to investigate the circumstances of the loss, verify the insured's compliance with policy conditions and security warranties, assess the value of the lost or damaged items, and determine the amount payable under the policy.

For high value claims, the investigation may involve forensic analysis (examining alarm systems, CCTV footage, vault access records), interviews with employees and witnesses, and engagement of specialist gemological valuers. The process is necessarily thorough, because the nature of the insured goods makes Jewellers Block particularly susceptible to exaggerated or fraudulent claims.

Valuation Disputes

One of the most common areas of contention in Jewellers Block claims is the valuation of lost items. The insured may claim that a lost diamond was worth $100,000 based on their own records and replacement cost. The insurer's valuer may assess it at $70,000 based on wholesale market conditions and a different grading assessment. Resolving these disputes fairly requires expert gemological knowledge, access to current market data, and a commitment by both parties to the principle of indemnity: restoring the insured to their pre-loss position, not enriching them and not short changing them.

Subrogation and Recovery

After paying a claim, the insurer has the right of subrogation: the right to pursue recovery from any third party responsible for the loss. If goods were stolen while in the custody of a courier company, the insurer may pursue the courier for failing to provide adequate security. If goods were damaged by a negligent setter, the insurer may recover from the setter. In international transit claims, subrogation can involve complex cross-border legal proceedings and the application of international conventions governing carriage of goods.

Reinsurance and Capacity: The Capital Behind the Coverage

Jewellers Block is a class where individual losses can be very large. A single armed robbery of a high street jeweller can generate a claim of $500,000. A theft from a trade exhibition can run into millions. The catastrophic scenario, a major robbery of a vault or a loss during a high value international transit, can produce claims that challenge the capacity of any single insurer.

This is why structured reinsurance is essential to the Jewellers Block market. Primary insurers cede a portion of their risk to reinsurers, who in turn may cede portions to retrocessionaires, creating the layered capital structure that we explored in Blog 2. Reinsurers evaluate Jewellers Block portfolios with particular scrutiny, focusing on aggregation control (how much value is concentrated in any single location or transit), maximum line per risk, catastrophe exposure (what happens if a major exhibition venue is robbed or destroyed by fire), and the insured portfolio's overall compliance with security requirements.

For the insured, the strength and stability of the reinsurance arrangements behind their policy is not an academic concern. It determines whether the insurer has the financial capacity to pay a large claim promptly and in full, without dispute or delay. Coverage backed by Lloyd's syndicates and “A” rated reinsurers provides the highest level of assurance. It is worth noting that Lloyd's of London provides a unique additional layer of security through its Central Fund, which acts as a capital backstop ensuring that valid claims are paid even if a specific syndicate cannot meet its liabilities. For a merchant whose entire livelihood may be sitting in a single vault, this capital certainty is not a marketing point. It is a non-negotiable requirement.

Risk Profile by Trade Segment

| Trade Segment | Risk Level | Primary Exposures |

|---|---|---|

| Retail Jeweller (High Street) | High | Armed robbery, smash and grab, shoplifting, employee dishonesty, display risk |

| Wholesale / Trading House | High | Transit risk, consignment exposure, credit risk on memorandum sales, employee infidelity |

| Diamond Dealer / Cutter | Moderate to High | Transit between cutting centres, mysterious disappearance, valuation disputes, substitution |

| Gold Bullion Dealer | Moderate to High | Price fluctuation, transit risk, vault security, large single consignment exposure |

| Manufacturing / Workshop | Moderate | Fire and accidental damage, employee handling errors, work in progress valuation |

| Auction House | Moderate | Exhibition display risk, transit of consigned goods, authentication and provenance disputes |

| Pawnbroker | High | Robbery, valuation accuracy, pledged goods custodianship, customer dispute |

The Jewellery Insurance Market in Southeast Asia

Southeast Asia occupies a unique position in the global jewellery trade. Thailand is one of the world's largest gemstone cutting and trading centres. Myanmar remains a primary source of rubies, sapphires, and jade. Indonesia has a significant gold mining and refining industry. Singapore functions as a trading hub for precious metals and high value goods. Malaysia, Vietnam, and the Philippines have growing domestic jewellery retail markets driven by rising middle class wealth.

Despite this concentration of trade activity, insurance penetration in the jewellery sector across the region remains surprisingly low. Many jewellers, particularly smaller operators in traditional markets, rely on physical security (vaults, guards, family oversight) rather than formal insurance. Some are unaware that Jewellers Block insurance exists. Others perceive it as prohibitively expensive or unnecessarily complex.

This protection gap mirrors the pattern we observed in medical malpractice in Blog 4. The risks are real and growing (organised crime targeting jewellery premises, increasing transit volumes, the expansion of online jewellery sales), while insurance adoption lags behind. Closing this gap requires not just product availability but education, accessibility, and trust.

Regulatory and Cultural Considerations

The jewellery trade in Asia is culturally distinct from its European and American counterparts. Many businesses are family owned, multi-generational, and operate on the basis of personal trust and verbal agreements. Stock may be held on memorandum (consignment) with minimal written documentation. Valuations may be based on internal knowledge rather than formal appraisals. Record keeping practices vary enormously.

For underwriters, these cultural factors are not obstacles. They are realities that must be understood and accommodated within the underwriting framework. A Jewellers Block policy designed for the London market cannot simply be transplanted to Bangkok or Mumbai. The terms, conditions, security requirements, and claims procedures must be adapted to the way the trade actually operates in each market, while maintaining the underwriting discipline that the class demands.

Technology and the Future of Jewellers Block

The jewellery insurance sector has historically been one of the most traditional and paper-intensive in the specialty market. But technology is beginning to transform every aspect of the value chain.

Digital Inventory and Stock Management

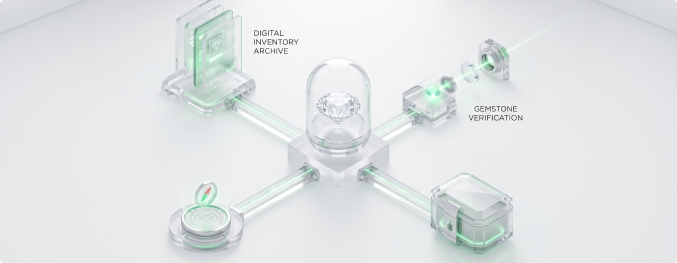

Accurate, real-time stock records are fundamental to both underwriting and claims. Digital inventory management systems that track every item from acquisition through to sale, recording its location, custodian, valuation, and photographic record, provide the evidentiary foundation that Jewellers Block underwriters and claims adjusters require. The transition from handwritten stock books to digital platforms is one of the most important developments in improving the insurability of jewellery businesses.

Computer Vision and Gemological Verification

Advances in computer vision and artificial intelligence are enabling automated verification of gemstones and finished jewellery. Photographic records taken at the time of insurance can be compared algorithmically against items presented in a claim, assisting in the identification of substituted or misrepresented stock. While the technology is not yet a replacement for expert gemological assessment, it is a powerful supplementary tool for both underwriting verification and claims investigation.

GPS Tracking and Transit Security

Real-time GPS tracking of high value consignments during transit provides underwriters with visibility into the most vulnerable phase of the supply chain. Tracking data can trigger alerts if a shipment deviates from its planned route, enters an unauthorised area, or remains stationary for longer than expected. This real-time risk monitoring represents a shift from retrospective claims management to proactive risk prevention.

Hardware Integrated Insurance: The Next Frontier

Perhaps the most transformative development in specie insurance is the convergence of physical security hardware with insurance logic. Innovations in this space include secure transit receptacles equipped with GPS and GSM sensors that do not merely contain high value goods but track them in real time, communicating location and status to a central platform.

Some systems incorporate Intelligent Banknote Neutralisation Systems (IBNS), where a breach of the secure container triggers an ink stain mechanism that renders bank notes invalid and useless to thieves. This technology dramatically reduces the incentive for theft and fundamentally changes the risk calculus for the underwriter. When the stolen goods are rendered worthless at the moment of theft, the nature of the risk transforms from a high severity exposure to a deterrence-driven model.

This hardware integration also enables a shift from static annual policies to dynamic, on-demand coverage. Rather than purchasing an annual policy with a fixed carry limit, a cash-in-transit operator can secure insurance for a single trip via a digital platform. The insurance module calculates the risk based on the specific route, time of day, value of the consignment, and the security features of the transit system. This pay-per-trip model matches insurance cost to actual risk exposure, making coverage more accessible and more economically efficient, particularly for smaller operators who previously could not justify the cost of annual policies and armoured courier services.

Digital Platforms and Accessibility

Specialist InsurTech platforms are making Jewellers Block insurance more accessible, particularly for small and medium-sized jewellers who have historically found the class too complex or too broker-dependent to access. Digital platforms that allow jewellers to obtain quotes, customise coverage, manage certificates, and report claims online are lowering the barriers to entry and expanding insurance penetration across the trade. In Southeast Asia, where the protection gap is particularly pronounced, digital accessibility is a critical enabler.

Data Intelligence and Portfolio Analytics

As specialist portfolios grow, the data they generate becomes increasingly valuable. Portfolio analytics can identify anomaly patterns (unusual claims frequency from specific regions or trade segments), concentration risk (too much exposure aggregated in a single geography or exhibition), transit frequency trends, and loss clustering that may indicate systemic security weaknesses or emerging criminal activity.

Artificial intelligence supports pattern recognition at a scale and speed that human analysis cannot match, but underwriting judgement remains central. Data intelligence informs the underwriter's decision; it does not replace it. The most sustainable portfolios are those where technology and human expertise work in concert: algorithms flagging anomalies, underwriters interpreting them, and the resulting insights feeding back into risk selection, pricing, and security advisory.

Embedded and Integrated Risk Models

The most significant long-term development in jewellers block and specie insurance may be the emergence of embedded risk models. When logistics protocols, insurance coverage, real-time data capture, and claims handling all operate within a unified framework, something transformative happens: information asymmetry between insurer and insured reduces dramatically. The underwriter's assumptions about security compliance, transit protocols, and stock management are verified by operational data in real-time, rather than relying on self-reported declarations once a year at renewal.

This integration creates a virtuous cycle. Better data leads to more accurate underwriting. More accurate underwriting leads to fairer pricing. Fairer pricing attracts better risks. Better risks produce lower claims. And lower claims sustain stable, long-term capacity in a class where capacity is hard won and easily lost.

The Human Element: Trust in a Digital Age

Despite the rise of AI, IoT, and digital platforms, the jewellery and specie insurance market remains, at its heart, deeply human. Trust is the currency of the trade.

In industries like the diamond market, deals have historically been sealed on a handshake. A dealer's word is their bond, and a reputation built over decades can be destroyed by a single breach of trust. Insurance platforms serving this market must mirror that ethos. Digital efficiency must not come at the cost of human support. The most successful specialist providers in this space maintain dedicated teams for complex claims, ensuring that a jeweller who has suffered a devastating robbery is not left facing automated responses and chatbot menus during the worst moment of their professional life.

There is also an important educational role for technology. Digital platforms can use interface prompts to remind policyholders of critical conditions and exclusions at the point of transaction. For example, a reminder about the unattended vehicle clause (which typically excludes theft if goods are left in a vehicle, even briefly) displayed at the moment a transit is being arranged can prevent a claim from ever arising. This proactive, embedded education is one of the most valuable and least celebrated functions of InsurTech in the specialty market.

What to Look for in a Jewellers Block Provider

For jewellers evaluating their insurance options, and for anyone seeking to understand the quality of a jeweller's protection, these are the critical factors. Coverage should always be evaluated on the basis of security warranty clarity, transit limit adequacy, territorial scope, claims governance, and reinsurance backing, rather than on premium alone. The cheapest policy is, in this class more than most, frequently the most expensive one when a claim arises.

Specialist trade knowledge. Does the insurer or Coverholder understand the jewellery trade? Can they discuss vault specifications, transit protocols, exhibition security, and consignment practices with fluency? Generalist insurers who treat jewellery as just another property class will produce inadequate coverage and frustrating claims experiences.

All risks breadth with clear conditions. The policy should be genuinely all risks, with exclusions that are clearly stated and understandable. Ambiguity in policy wording is the source of most disputes at the time of a claim.

Appropriate territorial scope. The policy must cover every jurisdiction where the jeweller's stock travels. A single uncovered transit can result in a total loss with no recourse.

Specialist claims adjusters. When a loss occurs, the adjuster must have gemological expertise and trade knowledge. A property adjuster who normally handles building damage is not equipped to value a parcel of loose sapphires or investigate a mysterious disappearance.

Security advisory capability. The best providers do not just insure jewellers; they help them improve their security. Pre-risk surveys, security recommendations, and ongoing advisory support reduce claims frequency and benefit both insurer and insured.

Financial strength and Lloyd's backing. Jewellers Block claims can involve large single loss amounts. The insurer must have the capital strength to pay significant claims without delay. Lloyd's syndicates and “A” rated carriers provide the highest level of financial security.

Closing the Series: A Hidden Gem That Touches Every Life

This blog brings the Insurance Decoded series to its close, and it is fitting that it ends with one of the most specialised and fascinating classes in the global insurance market.

Across five instalments, we have traced a journey from the foundational principles of insurance (Blog 1) through the ecosystem of players and intermediaries (Blog 2), the full taxonomy of insurance types and the technologies reshaping them (Blog 3), the complex and deeply human world of medical malpractice and its role in the healthcare ecosystem (Blog 4), and now the specialised domain of Jewellers Block and Specie insurance.

The thread that connects every instalment is the same: insurance, properly understood, is not a grudge purchase or a bureaucratic formality. It is the architecture of protection that allows individuals, businesses, and entire industries to operate with confidence in an uncertain world. It is the mechanism by which society shares the burden of risk so that no single person or entity is destroyed by a loss that could happen to anyone.

The principles are timeless: utmost good faith, indemnity, insurable interest, contribution, subrogation, proximate cause. The ecosystem is vast: from the policyholder to the reinsurer, from the agent to the actuary, from the regulator to the retrocessionaire. The products are diverse: from a simple term life policy to a complex Jewellers Block programme covering stock across twelve countries. And the technology is transformative: making insurance faster, fairer, more accessible, and more responsive than at any point in its long history.

The future of Jewellers Block and Specie insurance, and indeed of insurance more broadly, lies in what some commentators are calling the “phygital” convergence: the merging of physical security (secure vaults, IoT-tracked containers, IBNS deterrence systems) with digital intelligence (AI underwriting, real-time data analytics, embedded policy logic). The static, annual contract is giving way to dynamic, data-driven coverage that matches insurance cost to actual risk exposure in real time. The Fort Knox of the future is no longer just steel and concrete. It is software, sensors, and smarter risk transfer.

What has not changed, and what must never change, is the fundamental purpose. Insurance exists to make people whole. It exists to investigate claims honestly, to compensate loss fairly, and to sustain the trust upon which commerce and community depend.

An Invitation

This series has been my attempt to open a door into an industry that touches virtually every aspect of modern life yet remains, for most people, a black box of jargon, fine print, and opaque processes. Insurance is, in many ways, a hidden gem: quietly underpinning the confidence with which we build businesses, practise professions, transport goods, and plan for the future. My hope is that these five instalments have made that hidden gem a little more visible.

I do not pretend to have covered every nuance or answered every question. Insurance is a vast and evolving field, and I am still learning every day. If you have feedback, questions, or perspectives that could deepen or challenge what I have written here, I welcome them sincerely. If you see opportunities for collaboration, whether in education, in product development, in research, or simply in conversation, I am open to them. The best ideas in this industry have always come from the intersection of different perspectives, and I believe there is far more to learn from listening than from lecturing.

On a personal note, one of the quiet motivations behind this series was a hope that my own family might finally understand what I do for a living. For years, the answer to “What does Appa do at work?” has been met with polite nods and glazed eyes. If this series has made the world of insurance even slightly more accessible and comprehensible, then perhaps the next family dinner will be a little less mysterious.

I hope so, at least.

Thank you for reading. It has been a privilege to share this journey with you.

Disclaimer: The opinions expressed herein are solely those of the author in his personal capacity and do not reflect the views of JA Assure Group, Lloyd's of London, or any associated syndicate or partner.